Why Portfolio Managers Queue for a Blackstone Pitch

The part of Blackstone's playbook that doesn't require being Blackstone.

Hi! This is George from Orama, I’m restarting this newsletter with a new purpose. Sharing what I see working in content and thought leadership for firms who sell complex solutions to financial institutions. If it's not useful, you can unsubscribe here.

At the bottom of this email you’ll find:

A round up of what I’ve been reading recently on enterprise sales, “Signals”

Podcast appearance opportunities

I just came back from an Easter break near Geneva, where I met an ex-client, now a friend, for a beer after work by the lake. He works at one of the largest independent asset managers the city is known for. He mentioned something unusual from that day: portfolio managers and client advisors were crowding a meeting room because a Blackstone executive was visiting the office.

Blackstone is a huge brand, the largest alternative asset manager on the planet. Their products are in demand. But a visit is still a pitch. And these people get pitched constantly — including by Blackstone’s direct competitors with similar products. I used to cover them in my early sales days, they don’t rush to meetings.

So why this one?

In institutional sales, the firm that closes the deal isn’t always the best — it’s the most familiar. Before the Blackstone executive books the meeting, they've seen him or his colleagues twenty times, and they feel they know him. The conversation started from familiarity, not zero. That's the moat — and it's been engineered.

How Blackstone engineers familiarity at scale

It's easy to dismiss Blackstone's video output as retail marketing. BCRED, their private credit fund for individuals, has grown from zero to over $80 billion since 2021. Of course they're on LinkedIn now. But the formats themselves — the executives featured, the questions asked, the topics covered — are built for institutional buyers. Retail sees them as a byproduct.

Jon Gray jogging while giving a market update.

Managing directors answering questions pulled from a jar.

Executives interviewed between meetings.

Blackstone ensures they create familiarity through specific, repeatable formats. The executives featured are the ones pension funds and family offices actually meet with.

Familiarity ensures that when you finally do make the shortlist, you arrive as a known peer rather than a total stranger.

Take this one.

Martin Brand, Head of Blackstone Capital Partners, is “between two meetings”. It’s well-rehearsed but feels natural. The cameraman is addressed with a “you again”, which makes the interaction feel familiar — and by extension, so does the audience.

The script itself? Where Blackstone is allocating capital. How they work with portfolio companies. These are questions an institutional investor could ask in a meeting.

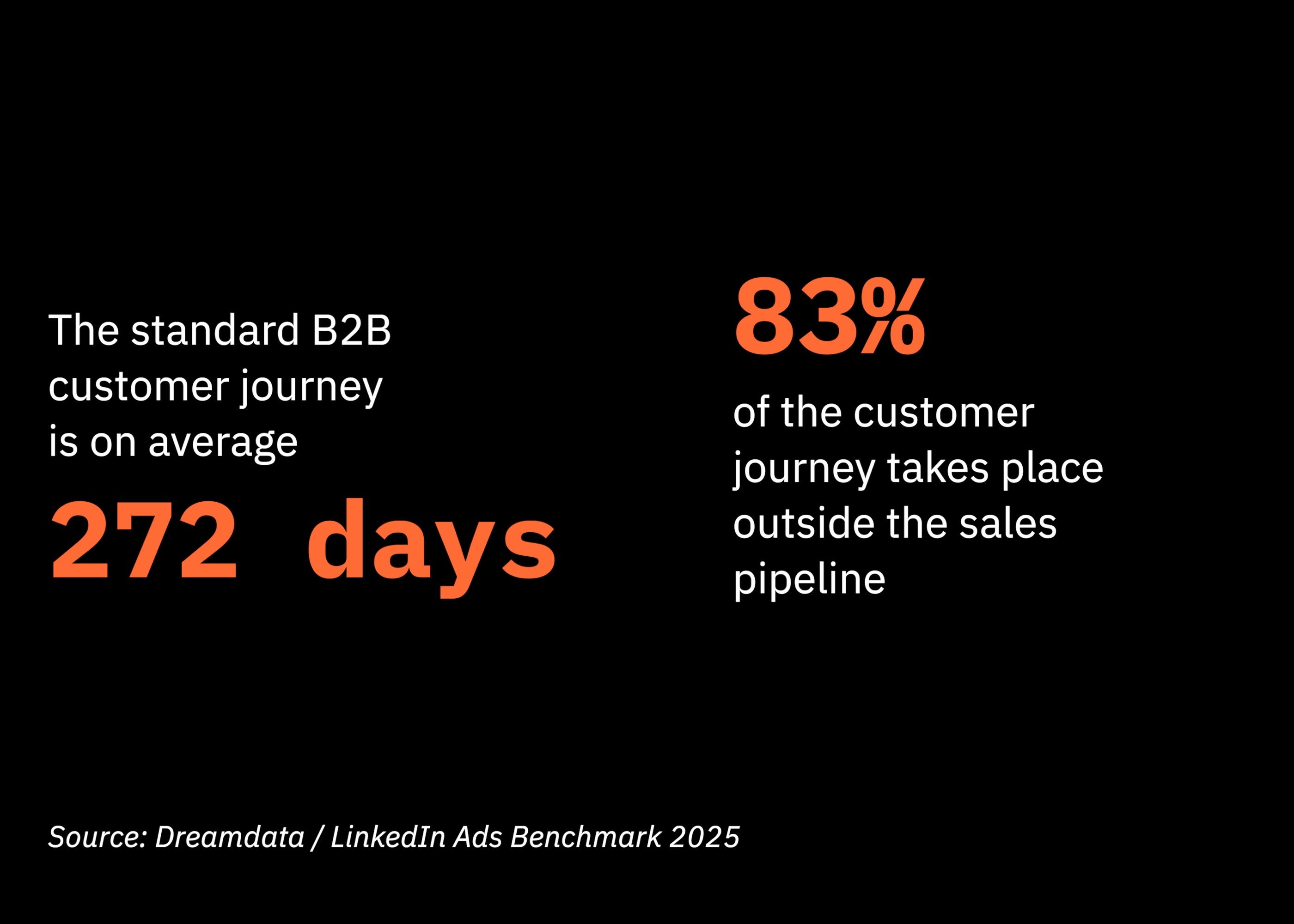

B2B buyers conduct the vast majority of their research before a salesperson ever gets a call. None of this replaces Blackstone’s 100-page offering memorandum or the sleek deck. It runs alongside them.

This isn’t traditional content marketing. The thought leadership is a given. It’s a familiarity engine for enterprise sales — and it requires formats, series.

Format is architecture

This isn’t unique to Blackstone. JPMorgan runs repeatable formats like “Minute on the Market”, or the one where they pull questions from a jar. Same pattern, same goal: make senior buyers feel like they already know the speaker before the meeting happens.

A format is a piece of architecture. You build it once: the setting, the constraint, the sequence, and then you run content through it, episode after episode. It’s primarily associated with TV and light entertainment, but operas, conferences also have their formats. Familiarity rewards repeat viewing. And repeat viewing reinforces the perception of reliability and integrity. Which leads to trust.

We conceptualize trust as existing when one party has confidence in an exchange partner’s reliability and integrity.

(Morgan and Hunt, Commitment-Trust Theory of Relationship Marketing)

But when it comes to enterprise sales, this only works if your content is designed for the buying committee. Their purpose is to carry your thought leadership. The greatest risk is developing a popular format where you can’t fit the right content.

Views are usually a vanity metric. But enterprise sales don't close with a click — they close after months, through committees. You can't attribute a signed deal to a specific article or post. So when a content built for your CTO buyer persona gets watched, the vanity becomes a signal.

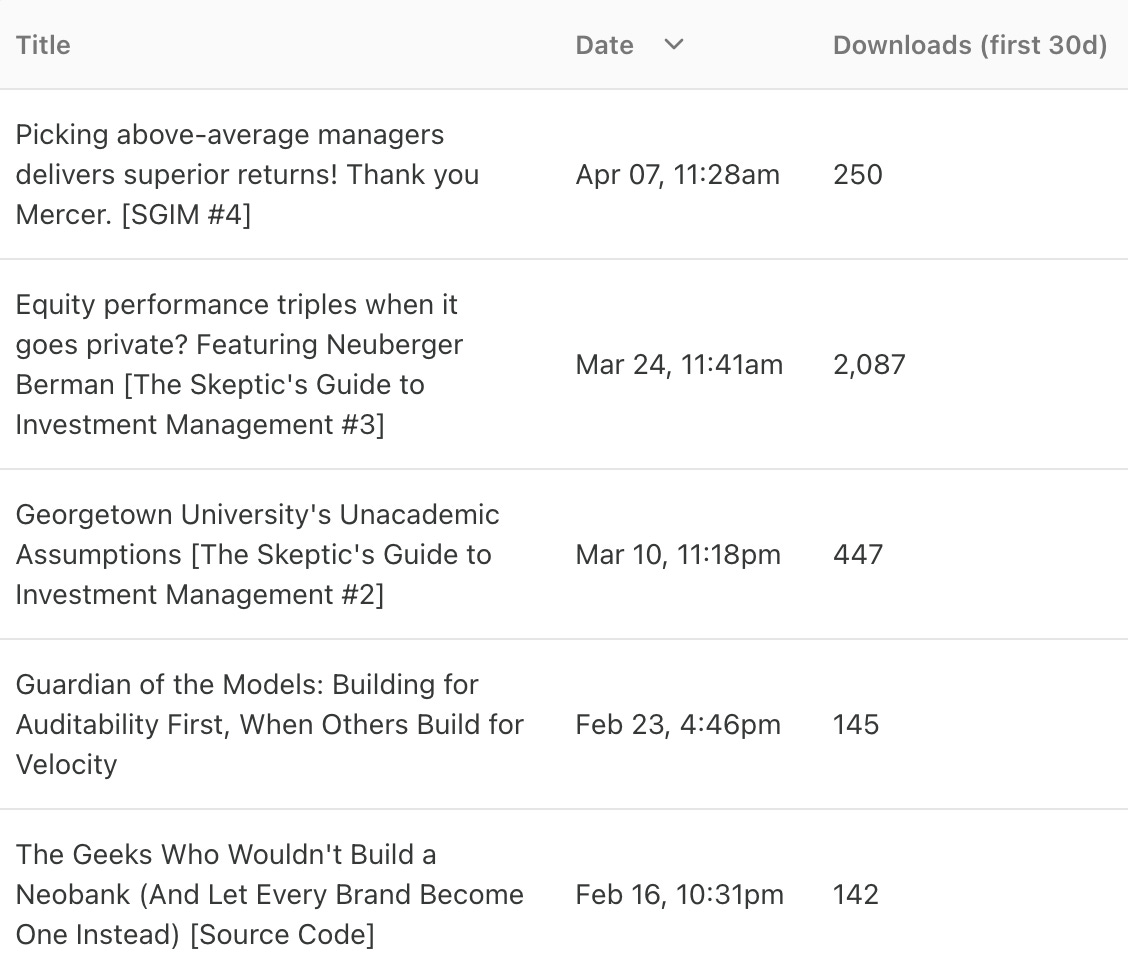

I’ve seen this in my own experiments. The Investorama YouTube channel reached 20k subscribers, but growth only started once we introduced a familiar narrative structure. More recently, on the Investology podcast, our “Skeptic’s Guide to Investment Management” draws significantly more downloads per episode, without promotion.

The “Skeptic” angle, is signalling a shared worldview.

The takeaway for selling to financial institutions

The C-suite you're selling to is already making content for their own buyers — or watching their colleagues do it.

For enterprise fintechs, expertise never was a problem. Most already have whitepapers, webinars, podcasts. What's missing is the format that connects it to the sales cycle. They're optimizing for substance without familiarity. Blackstone optimized for both.

How Orama can help

If you’re selling to financial institutions, familiarity isn’t a byproduct.

That’s the gap we build for.

We start from the buying committee, not the content calendar. What each stakeholder needs to hear, and when they need to hear it. Two things make this work:

Market Intelligence — We monitor what institutional buyers are actually paying attention to, and feed it into every piece of content.

Conversation Architecture — Our method for turning expertise into formats that build familiarity across the sales cycle.

Signals

What I’ve been reading on enterprise sales recently.

People

A $250K video director role for Anthropic: Worth noting what the job spec reveals about how Anthropic thinks about go-to-market. Video is strategic but this pays less than OpenAI’s storytelling job ($400K).

DACH B2B SaaS Has a Marketing C-level Gap: CMOs remain rare in B2B SaaS. Many companies aren’t yet at the scale where a CMO feels essential, while others still treat marketing as a complementary function and opt instead for a Chief Sales or Commercial Officer. My guess is this is even more acute in B2B Fintech. (The Big Byte)

Moves

Plaid acquires TWIF: A payments infrastructure company buying a media brand. When your product is complex and your buyers are everywhere, owning the conversation beats renting it. I didn’t see TWIF as having a massive brand or audience, but Plaid must have done the maths vs building their own.

Open AI acquires TBPN: Same logic. Here the question is the price “low hundreds of millions” for a YouTube channel with 60k subscribers?! Mine has 20k and I’ve received an offer once, but it was not in millions. By the way, TBPN is a format machine, across platforms. Check out their cards.

Fairmint acquires The RWA Desk: Again, it looks like owning a niche media is faster/cheaper than building an audience from scratch. Some B2B brands are starting to treat media as infrastructure.

Perspectives

AI: Iterate on the plan not the product: "spec, generate, evaluate, revise spec, regenerate" rather than "generate, edit, edit, edit." This resonates deeply, I’m trying to make it a rule when dealing with LLMs. It’s very tempting to go to the results first. Very applicable to… Formats.

Go Fast, Go Laterally, or Go Home: Thoughtful piece of advice for challenger brands in the financial industry.

Podcast guests wanted

Relaunching two series after a break. Looking for guests who fit:

Unsloppable — for marketing and enterprise sales leaders with a point of view on selling the complex against the slop.

Investology — for founders, operators, and investors using or providing investment management technology.

If you’re a fit — or know someone who is — reply to this email or book a call with me.

Written between meetings.

George